5

Non-competing strategy to focus on areas where it is difficult for the major players

Demand is attracted to technologies professionally developed for commercial use

The competitive landscape for Artificial Perception (AP) is very different from that for Artificial Intelligence (AI), making it easier for a selected small elite team to be competitive.

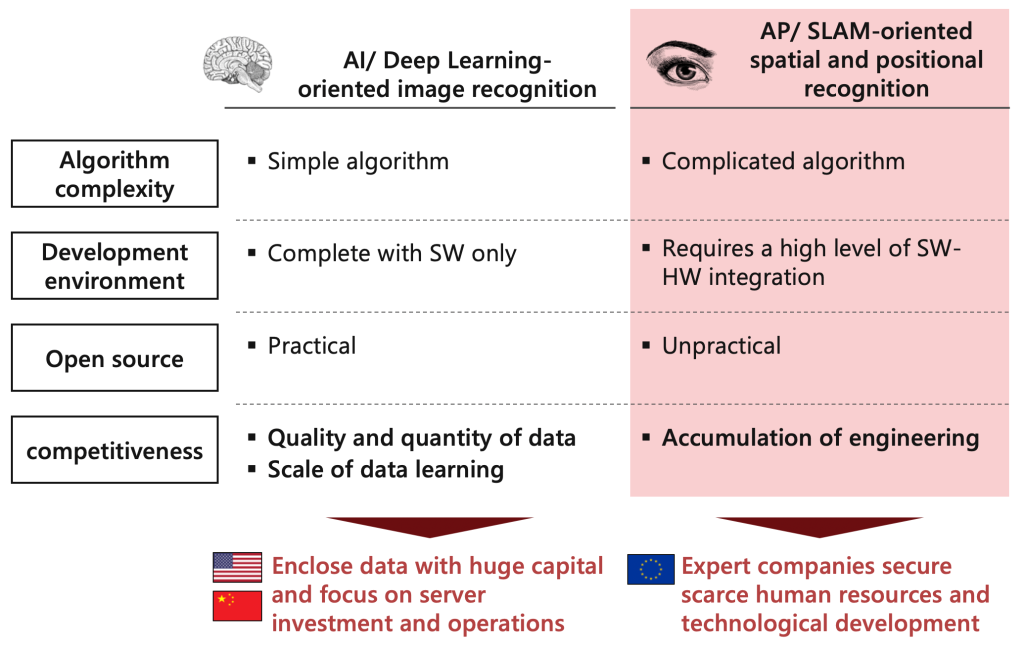

Artificial Intelligence (AI) is very simple as algorithms, and open source is also available mainly from major companies, so there is no fierce competition at the algorithm level. However, on the other hand, it requires the quantity and quality of data for data learning (reference link), which determines performance, and computing resources to handle the huge amount of data learning are required. Against this backdrop, the US and Chinese tech giants, with their overwhelming capital power, are competing with each other by investing huge amounts of money in data enclosures, servers and other computing resources and their operation.

Artificial Perception (AP), on the other hand, is a major challenge, as the algorithms are thousands of times more complex than Artificial Intelligence (AI). The development environment, including hardware, is essential, making open source impractical and developing the algorithms themselves a significant challenge. To compete in such complex algorithms technology, the key factor is to accumulate steady technological development, and specialised companies such as Kudan can be competitive by securing scarce human resources to develop them.

There are also regional differences. In the US and China, with their tech giant using their capital strength to focus on Artificial Intelligence (AI), where demand is rising quickly, and Europe is at the forefront in the relatively niche area of Artificial Perception (AP).

Non-competing segregation has progressed, making Kudan the largest independent specialist in the world

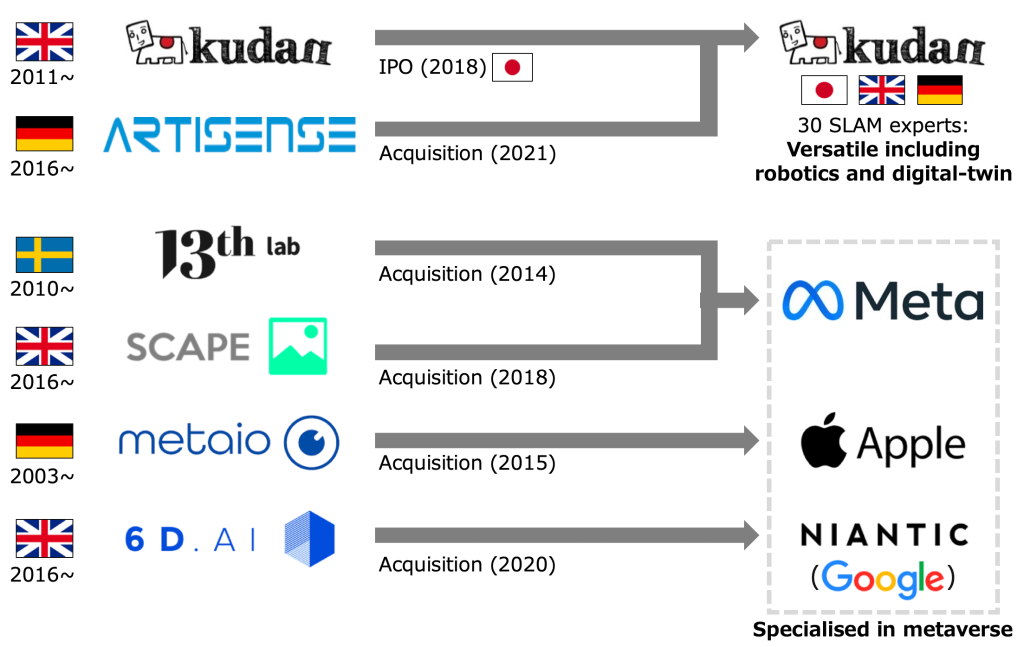

The Artificial Perception (AP) start-ups that have emerged mainly in Europe, many of which came into existence in the 2010s, have seen considerable progress in segregation and consolidation.

As major moves, many of the so-called GAFA tech giants have acquired start-ups with the aim of applying them to the metaverse. Enclosure as spatial technology for Augmented Reality (AR) and Virtual Reality (VR) has occurred, and these technology streams have led to products such as Meta’s Quest and Apple’s Vision Pro, for example.

Meanwhile, through acquiring Artisense, Kudan became the world’s largest group of independent, dedicated tech vendor as a leader for general-purpose technologies other than the Metaverse, such as robotics and digital-twin. Kudan now has around 30 specialist engineers specialising in Artificial Perception (AP) in the group, making it the largest team in the world concentrating on the deepest technology in the field.

Establish de facto standard technologies in the markets where the large players cannot easily fit

Through this segregation and integration, Kudan is gaining a foothold in areas that are difficult for large tech companies to enter.

As mentioned above, the giant tech companies are focusing more on the metaverse and, due to the nature of their business domains, competition is intensifying around consumer products and services. Kudan, on the other hand, focuses on robotics and digital-twin for enterprises and industries, including many private spaces. End customers in these domains value the use of their own systems and the confidentiality and ownership of their data, making it difficult for companies like GAFA, which compete with their customers for data, to enter the market. Dedicated companies like Kudan, which can act as a deep technology vendor without conflicting with the interests of their end customers, are valued.

While the market is still open and challenging for large companies to enter, Kudan aims to establish and spread de facto standards.